The Property Tax Reality Overseas Buyers Face in Spain

|

|

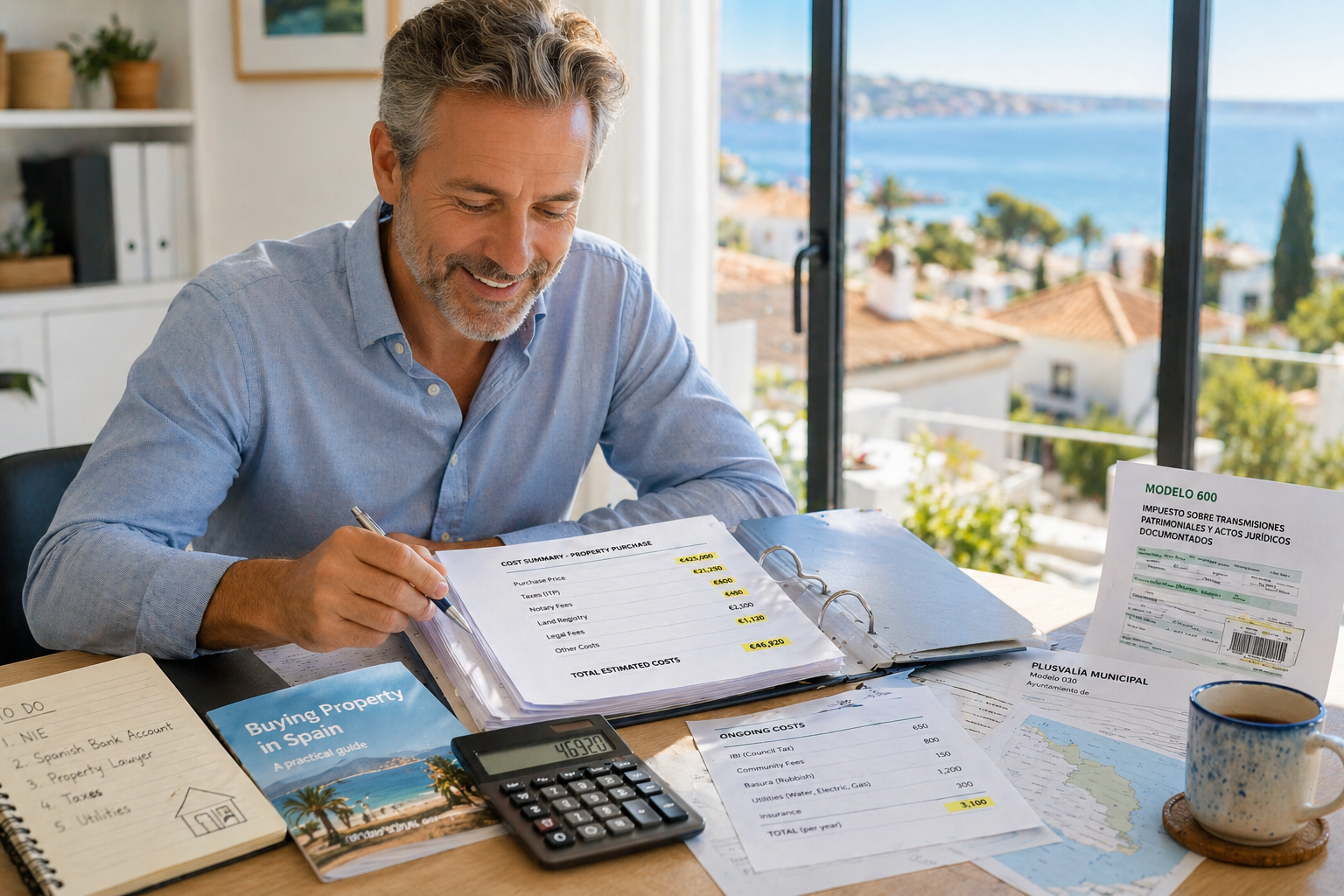

Buyers often enter the Spain property process focused on purchase price and lifestyle appeal, only to discover that taxes reshape the real cost picture once ownership begins. Initial excitement around a coastal apartment or inland villa gives way to questions about annual bills, transfer taxes paid at completion, and future liabilities when selling. This shift from headline price to full ownership costs creates one of the most common points of hesitation and budget recalibration.

This friction arises because overseas buyers naturally prioritise visible elements — location, views, finishes — while tax structures operate on less transparent metrics like cadastral values, municipal rules, and regional variations. Spain’s system layers one-time acquisition taxes with recurring municipal charges and potential non-resident income tax implications. What looks like a straightforward 8–12% buying cost quickly fragments into multiple payments across different authorities and timelines.

A key behavioural pattern emerges here too. Remote research often relies on average figures or agent summaries that underplay regional differences. A buyer comparing Andalusia and Valencia listings may not realise how IBI rates, Plusvalía calculations, or transfer tax percentages diverge, leading to late-stage surprises that force budget adjustments or property reconsideration.

The timeline and decision impact is significant. Unaccounted tax liabilities can delay notary completion if funds fall short, or create post-purchase cash flow pressure. Buyers who treat taxes as an afterthought often face tighter liquidity exactly when setting up utilities, community fees, and potential rental compliance.

An overlooked consequence involves long-term ownership planning. Non-residents may encounter imputed income tax on unused properties, while future sales trigger capital gains and municipal Plusvalía. These elements compound if buyers assume Spanish rules mirror their home country’s systems.

Buyers Usually Overlook

- How cadastral value (often 30-50% of market value) drives IBI, not the price you paid.

- Regional transfer tax variations (ITP 6-13% on resales depending on the autonomous community).

- The need for a fiscal representative for non-residents to handle annual filings.

- Plusvalía Municipal on sale, calculated on land value increase.

- Potential wealth tax exposure above certain thresholds.

Practical Tax Awareness Framework – Before You Proceed

- Request the current IBI receipt and cadastral reference during early viewings.

- Ask your independent lawyer for a full tax breakdown (acquisition + first-year recurring) specific to the property and municipality.

- Factor 10–14% above purchase price for all buying costs, then model realistic annual ownership expenses.

- Clarify your residency status early — it affects income tax treatment and deductions.

- Build a 12–24 month cash buffer that includes taxes alongside maintenance.

This keeps tax realities from derailing momentum once emotional commitment is high.

|

|

Twitter

Twitter Facebook

Facebook linkedin

linkedin Google

Google